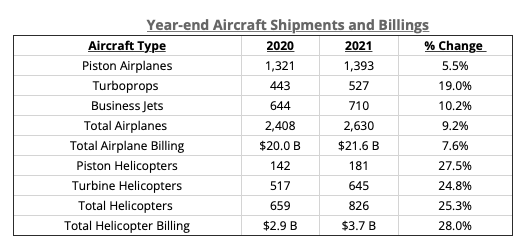

The General Aviation Manufacturers Association (GAMA) released the 2021 general aviation aircraft shipments and billings report during its annual state of the industry press conference. Overall, when compared to 2020, all aircraft segments saw increases in shipments and preliminary aircraft deliveries were valued at $25.2 billion, an increase of 10.2%.

“The strength and tenacity of the general aviation industry has provided a strong foundation for the industry to rebound from pandemic-related setbacks with a powerful showing in 2021. Total aircraft shipments are converging on figures that were seen before the outset of the pandemic. The industry has been able to weather the storm by strategically managing workforce and supply chain challenges, which unfortunately are still ongoing. Despite this adversity, there is robust interest and excitement in our industry as we continue to further our advancements in innovation, technology and environmental sustainability,” said Pete Bunce, GAMA President and CEO.

Airplane shipments in 2021, when compared to 2020, saw piston airplane deliveries increase 5.5%, with 1,393 units; turboprop airplane deliveries increase 19.0%, with 527 units; and business jet deliveries increase 10.2%, with 710 units. The preliminary value of airplane deliveries for 2021 was $21.6 billion, an increase of approximately 7.6%.

Piston helicopter deliveries for 2021, when compared to 2020, saw an increase of 27.5%, with 181 units; and preliminary civil-commercial turbine helicopter increase 24.8%, with 645 units. The preliminary value of helicopter deliveries for 2021 was $3.7 billion, an increase of approximately 28.0%.

The piston engine airplane market in North America accounted for 68.7% of overall shipments. The second largest market for piston airplanes for the seventh year in a row was the Asia-Pacific market at 14.4%. Turboprop airplane shipments to North American customers accounted for 52.6% of the global deliveries. The second largest market for turboprop airplane deliveries was the Latin American market at 15.7%. The North American market accounted for 65.9% of business jet deliveries. The second largest market for business jet deliveries during the year was Europe at 18.0%.

{kind=link}